Citi® Raises My Interest Rate from 8.24% to 14.99%

As a consumer with an 800+ FICO® credit score, I find it very vexing when a credit card bank raises my interest rate to that more suited to a subprime borrower, or someone with a limited or nonexistent credit profile. This has happened with a number of my consumer credit card accounts since the credit crisis peaked last year. In each case, I've opted out of the rate increase, which resulted in each account being closed by the bank.

Though I have the option to opt out of the latest assault on my credit -- an APR increase on my Citi® Dividend Platinum Select card -- I'm not going to. That's because this card has a relatively high credit limit, so closing this account would cause my FICO credit score to drop considerably. Keeping it open will not be a problem, as I haven't carried a balance on this card in years.

Change of Terms Notice

Since I will be accepting the change of terms. My APR will increase from 8.24% variable (Prime + 4.99%) to 14.99% variable (Prime + 8.99%, with a minimum of 14.99%) at the beginning of next month. In other words, in reality, my APR will rise to Prime + 11.74%! Simply outrageous for someone with my credit history. So why didn't Citi just note the change as Prime + 11.74% in the literature they sent me? Very good question. Perhaps it's because they know how uGlY it looks?

I'm betting that two years from now, when the Fed will be raising short-term rates to tame runaway inflation, the rate on this card will be close to 20%, if not higher. Just have a look at where the U.S. Prime Rate was at its most recent high: 8.25% from mid-2006 through September 2007.

Even more telling, let's plug in the median U.S. Prime Rate:

Yikes! Ouch! Just looking a those numbers makes me cringe.

Ok, so here is the reason I was given for the rate increase:

Citi's excuse is not so bad, however, when compared to the one Advanta gave me when they closed my business credit card account. That bank actually tried to paint me as a credit risk despite my high credit score, perfect payment record and my habit of paying at least three times the minimum amount due each month. Advanta has a lot of small business owners very angry, and I think that lawsuits and settlements are only just beginning for that company.

Ok, here's another quote from the change of terms notice:

As soon as I am done posting this blog entry, I will take my Citi® Dividend Platinum Select card out of my wallet, blindfold it, march it down to my crosscut shredder, give it its last cigarette and destroy it. I'll keep a record of the card's details, of course, just in case.

I'm actually grateful that banks like Citi exist. Why? Because my income varies so wildly that my credit union won't give me a credit card, despite my stellar credit rating. So, yeah, I like to complain when they're up to no good, but these banks actually play a vital role in providing credit to folks with undulating income, like me.

Though I have the option to opt out of the latest assault on my credit -- an APR increase on my Citi® Dividend Platinum Select card -- I'm not going to. That's because this card has a relatively high credit limit, so closing this account would cause my FICO credit score to drop considerably. Keeping it open will not be a problem, as I haven't carried a balance on this card in years.

Change of Terms Notice

Since I will be accepting the change of terms. My APR will increase from 8.24% variable (Prime + 4.99%) to 14.99% variable (Prime + 8.99%, with a minimum of 14.99%) at the beginning of next month. In other words, in reality, my APR will rise to Prime + 11.74%! Simply outrageous for someone with my credit history. So why didn't Citi just note the change as Prime + 11.74% in the literature they sent me? Very good question. Perhaps it's because they know how uGlY it looks?

I'm betting that two years from now, when the Fed will be raising short-term rates to tame runaway inflation, the rate on this card will be close to 20%, if not higher. Just have a look at where the U.S. Prime Rate was at its most recent high: 8.25% from mid-2006 through September 2007.

8.25% + 11.74% = 19.99%.

Even more telling, let's plug in the median U.S. Prime Rate:

8.75% + 11.74% = 20.49%.

Yikes! Ouch! Just looking a those numbers makes me cringe.

Ok, so here is the reason I was given for the rate increase:

Actually, the way I see it, the rate increase has more to do with the really bad mistakes Citigroup made during the recent housing/credit boom than it does with this recession we're in. Of course, the banks that messed up want consumers and taxpayers to pay for their mistakes, while top executives continue to take home massive bonuses. Seems to be the new American way of doing business on Wall Street.

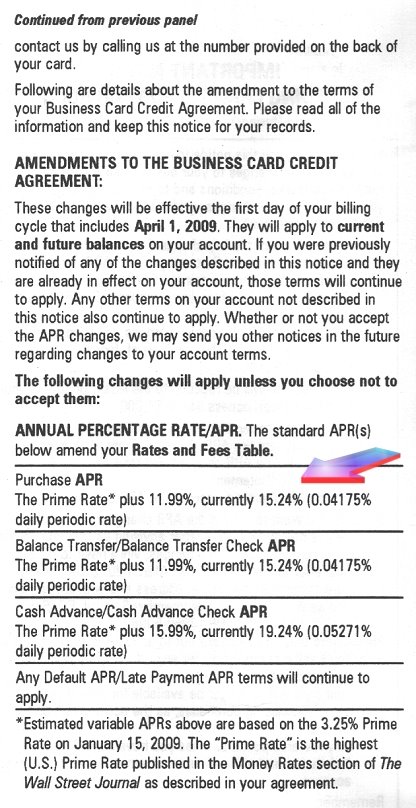

"...In this economic environment in order to continue to provide consumers with access to credit, we have had to adjust our pricing..."

Citi's excuse is not so bad, however, when compared to the one Advanta gave me when they closed my business credit card account. That bank actually tried to paint me as a credit risk despite my high credit score, perfect payment record and my habit of paying at least three times the minimum amount due each month. Advanta has a lot of small business owners very angry, and I think that lawsuits and settlements are only just beginning for that company.

Ok, here's another quote from the change of terms notice:

"...If you opt out of these changes, you may use your account under the current terms until the end of your current membership year or the expiration date on your card, whichever is later..."This is actually a much better policy than I've seen with other credit card banks. With other banks, when I opted out of rate increases, the bank either closed my account right away, or closed it within 30 days of my opting out. So, I will give some kudos to Citi for giving customers time to pay down their debt before jacking up their APR.

As soon as I am done posting this blog entry, I will take my Citi® Dividend Platinum Select card out of my wallet, blindfold it, march it down to my crosscut shredder, give it its last cigarette and destroy it. I'll keep a record of the card's details, of course, just in case.

I'm actually grateful that banks like Citi exist. Why? Because my income varies so wildly that my credit union won't give me a credit card, despite my stellar credit rating. So, yeah, I like to complain when they're up to no good, but these banks actually play a vital role in providing credit to folks with undulating income, like me.

Labels: banks, citi, credit_cards, credit_crunch, interest_rates

|

--> www.FedPrimeRate.com Privacy Policy <--

CLICK HERE to JUMP to the TOP of THIS PAGE --> SITEMAP <-- |

posted by Steve Brown | 7/23/2009 05:28:00 PM

![]()

![]()